Domestic Debt Servicing Gulps N19tn In Three Years

…Local Debt Rises By 262%, Servicing By 96% In Two Years

The Federal Government spent N18.86tn to service its domestic debts between 2023 and 2025, according to analysis conducted by THE WHISTLER.

Data obtained from the Debt Management Office showed that the Federal Government spent a total of N4.38tn to service its domestic debt in 2023.

The following year, the domestic debt spends rose to N5.87tn, showing an increase of 34.02 per cent within a period of 12 months.

By the end of 2025, the Federal Government spent a total of N8.61tn on domestic debt servicing. This reflects an increase of 46.68 per cent over the 2024 debt servicing expenses.

Thus, between 2023 and 2025 the cost of the Federal Government domestic debt servicing rose by N4.23tn, reflecting an increase of 96.57 per cent within a period of two years.

Advertisement

The data show a rapid escalation in Nigeria’s domestic debt servicing obligations between 2023 and 2025 as a result of increased total domestic debt burden.

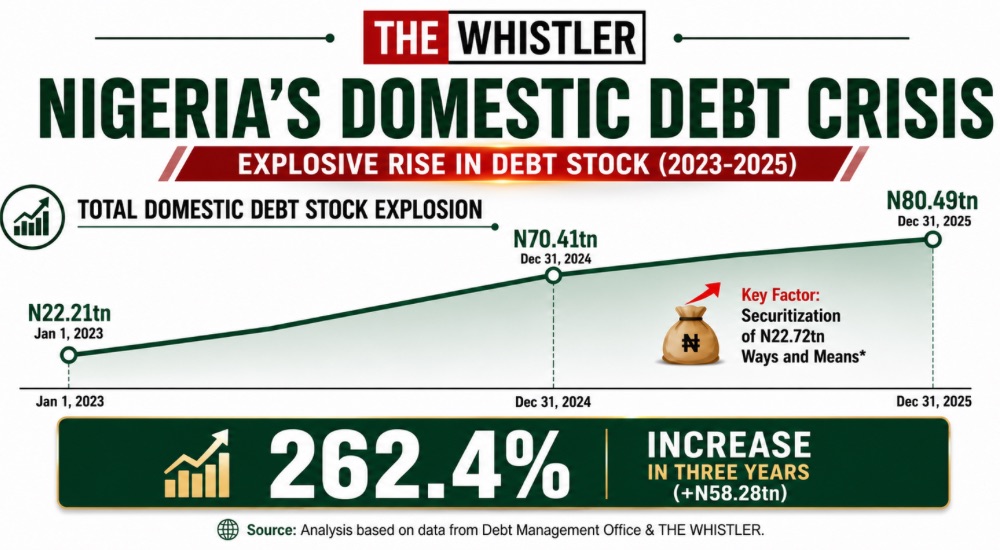

As of January 1, 2023, the domestic debt of the Federal Government stood at N22.21tn made up of N16.42tn FGN Bonds; N4.42tn Nigerian Treasury Bills; N50.99bn Nigerian Treasury Bonds; N27.51 FGN Savings Bond; 742.56bn FGN Sukuk; N15bn Green Bond; and N530bn Promissory Notes.

By December 31, 2024, the Federal Government’s domestic debt had risen to N70.41tn comprising N55,44tn FGN Bonds; 12.35tn Nigerian Treasury Bills; N992.56bn FGN Sukuk; N72.87bn FGN Savings Bond; N15bn Green Bond; and N1.54tn Promissory Notes.

As of December 31, 2025, the Federal Government domestic debt stock had risen to N80.49tn, comprising N63.63tn FGN Bonds; N13.85tn Nigerian Treasury Bills; N1.19 FGN Sukuk Bonds; N104.32bn FGN Savings Bonds; N62.36 FGN Green Bonds; N1.54tn Promissory Notes; and N100bn Unclaimed Funds Trust Fund FGN Security.

Thus, the domestic burden of the Federal Government rose from N22.21tn to N80.49tn between 2023 and 2025, showing an increase of N58.28tn or 262.4 per cent within a period of three years.

Advertisement

As a result of the increased local debt stock, total domestic debt servicing expenses increased sharply, from N4.38tn to N8.61tn in two years.

One of the items that increased the domestic debt burden of the Federal Government was the securitisation of the N22.72tn Ways and Means the Central Bank of Nigeria advanced to the government under the late Muhammadu Buhari.

Federal Government Bonds remained the dominant debt instrument throughout the three years, accounting for the largest share of debt servicing, although their share declined from 83.6 per cent in 2023 to 63.8 per cent in 2025.

Treasury Bills recorded the fastest growth, rising from N326bn in 2023 to N2.55tn in 2025, suggesting increased reliance on short-term domestic borrowing.

Promissory Notes consistently represented about four to five per cent of annual debt service.

Sukuk, Green Bonds and FGN Savings Bonds remained relatively small components of the domestic debt portfolio.

Advertisement

While Federal Government Bonds continued to dominate the local debt liabilities, the surge in Treasury Bills indicates a growing dependence on short-term financing.

The near doubling of total domestic debt service over the period suggests increasing fiscal pressure, with debt service consuming a much larger share of government resources than in previous years.

A breakdown of the debt servicing obligations for the three years under review shows that the interest on Nigerian Treasury Bills rose from N326.12bn in 2023 to N747.15bn in 2024 before rising to N2.55tn in 2025.

The servicing of FGN Bonds rose from N3.66tn in 2023. In 2024, it rose to N4.69tn before it peaked at N5.49tn in 2025.

On the other hand, N57.36bn was spent on servicing Treasury Bonds in 2023. Nothing was spent on this instrument in the subsequent years.

In 2023, the sum of N2.18bn was spent on servicing Green Bonds. The same amount was spent on the instrument in 2024. However, by 2025, the spending on the instrument rose to N6.67bn.

Green Bonds are specialised debt instruments which enables the Federal Government to borrow for the funding of environmentally sustainable projects such as renewable energy and clean transportation.

On Sukuk Bond, N103.25bn was spent in 2023. The spending on this Islamic financing instrument rose to N158.43bn in 2024. It rose again to N171.73bn the following year, 2025.

The FGN Savings Bond attracted an expenditure of N2.87bn in 2023. The expenditure rose to N6.38bn in 2024. By 2025, the expenditure had more than doubled again to N13.59bn.

The Federal Government uses the FGN Savings Bond to encourage small savers. It requires a minimum investment of N5,000 and offers fixed tax-free quarterly interests.

In 2023, a total of N226.17bn was spent on the redemption of Promissory Notes. This rose to N265.86bn in 2024 and to N370.93bn in 2025.

The Promissory Note is a legally binding document which the Federal Government issues to a creditor to pay a certain amount money on a future date. Sometimes, it is issued to contractors whose works have been verified for which the government lacks money to pay for immediately.

For the three years under review, the Federal Government spent N13.847tn on FGN Bonds; N3.624tn on Nigerian Treasury Bills; N862.96bn on Promissory Notes; N433.41bn on Sukuk; N57.36bn on Treasury Bonds; N22.84bn on FGN Savings Bond; and N11.02bn on Green Bonds.

Apart from increasing the debt obligations, experts have criticised rising operation in the domestic debt market on the grounds that it crowds out the private sector.

This is because government bonds are trusted investment instruments and because of safety, lenders tend to gravitate towards the government rather than the private sector.

The Minister of Finance and Coordinating Minister of the Economy, Taiwo Oyedele had last month urged Nigerians to stop viewing public borrowing as inherently negative, arguing that debt should be assessed by what it finances rather than its size.

Oyedele said the country’s long-standing aversion to debt has become a major obstacle to economic growth, investment mobilisation and business expansion.

According to him, borrowing should not be treated as a moral failure but as a financial tool capable of driving development when deployed responsibly.

He criticized what he described as the growing tendency by analysts and commentators to condemn every instance of government borrowing without considering whether the funds are being invested in productive projects capable of generating returns.

“The relevant question is never simply how much debt there is. It is always debt for what, at what cost, against what return and repayable on what terms,” he said.

Oyedele argued that governments and businesses that borrow to finance productive assets capable of generating returns above the cost of capital are acting rationally, adding that refusing to borrow under such conditions could amount to forfeiting valuable growth opportunities.

He also challenged Nigeria’s business culture, saying many entrepreneurs are reluctant to dilute ownership by bringing in external investors, even when doing so would enable their businesses to scale.

According to him, owning 100 per cent of a small enterprise often delivers less value than holding a significant stake in a much larger and better-capitalised company.

Beyond the issue of debt, the finance minister outlined what he described as the “seven laws of capital attraction,” stressing that investors are driven primarily by trust, policy consistency, strong institutions and the rule of law rather than generous tax incentives.

He said capital seeks predictable returns instead of simply chasing the highest returns, warning that countries with inconsistent policies often lose investors to jurisdictions offering lower but more stable returns.

“Capital hates uncertainty more than taxation,” he said, explaining that policy reversals, regulatory inconsistency, foreign exchange uncertainty and weak contract enforcement discourage investment more than moderate tax rates.