Despite FAAC Boom, Naira Crash Wipes Out Revenue Gains Under Tinubu

… Tinubu’s N47.8tn FAAC Allocation Worth Less Than Buhari’s N22.9tn In Dollar Terms

… Rising Costs, FX Depreciation Distort True Value Of FAAC Growth — Experts

An analysis of data sourced from the Office of the Accountant-General of the Federation (OAGF) and the National Bureau of Statistics (NBS) by THE WHISTLER has revealed that despite a sharp increase in Federation Account Allocation Committee (FAAC) disbursements under President Bola Tinubu, the real value of revenues shared among the three tiers of government has weakened significantly following the steep depreciation of the naira.

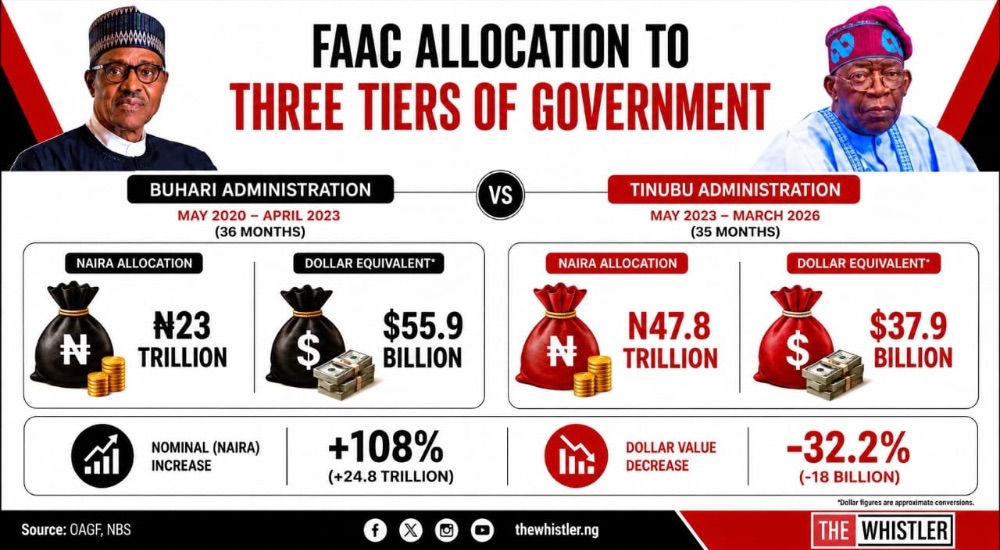

The findings showed that the federal, state and local governments collectively received N47.8tn from FAAC between May 2023 and March 2026 under Tinubu, compared to N23tn distributed during the last 36 months of former late President Muhammadu Buhari’s administration between May 2020 and April 2023.

The figures indicate an increase of N24.8tn in nominal naira terms under Tinubu’s administration. However, when adjusted for exchange-rate movements, the value of these allocations dropped sharply.

Analysis by THE WHISTLER showed that the naira averaged about N409.36/$ during the reviewed Buhari period but weakened significantly to an average of approximately N1,310.61/$ under Tinubu.

Advertisement

Using the Central Bank of Nigeria’s average monthly exchange rate during the Buhari administration and under Tinubu, the allocations translated to approximately $55.9bn under Buhari compared to about $37.9bn under Tinubu.

This represents a decline of roughly 32.4 per cent in dollar terms despite the substantial rise in naira allocations.

The analysis underscores the growing disconnect between nominal fiscal expansion and real value preservation amid Nigeria’s worsening inflationary pressures and currency volatility following major economic reforms introduced by the Tinubu administration.

Shortly after assuming office on May 29, 2023, Tinubu implemented sweeping reforms aimed at restructuring the Nigerian economy, including the removal of petrol subsidy and the liberalisation of the foreign exchange market.

During his inaugural speech, Tinubu famously declared that “subsidy is gone,” insisting that resources previously spent on fuel subsidies would be redirected into productive sectors and distributed more efficiently across the federation.

Advertisement

The administration also moved to unify the foreign exchange market, ending years of multiple exchange-rate windows that economists and investors had criticized for encouraging arbitrage, distortions and rent-seeking.

While the reforms triggered a sharp rise in federally collected revenues and monthly FAAC disbursements, they also accelerated the depreciation of the naira, weakened household purchasing power and pushed inflation to multi-year highs.

The depreciation substantially increased the cost of imported goods, infrastructure materials, foreign debt servicing and other FX-dependent government obligations across all tiers of government.

A detailed breakdown of the allocations revealed that the federal government received N9.6tn from FAAC during Buhari’s final 36 months in office, equivalent to approximately $23.6bn at the prevailing average exchange rate during the period.

Under Tinubu, allocations to the federal government rose sharply to N17.8tn between May 2023 and March 2026, representing an increase of approximately 85 per cent in naira terms.

However, when converted using the average exchange rate of N1,310.61/$ recorded during Tinubu’s administration, the allocation amounted to approximately $14.2bn.

Advertisement

This means that despite receiving significantly higher allocations in naira terms, the federal government experienced a 65 per cent decline in the real dollar value of FAAC revenues compared to the Buhari administration.

State governments also recorded a similar pattern.

Collectively, the 36 states received N7.6tn from FAAC between May 2020 and April 2023 under Buhari, equivalent to approximately $18.5bn.

Under Tinubu, allocations to state governments surged to N17.3tn, reflecting a 127 per cent increase in nominal naira terms.

Yet, after adjusting for exchange-rate depreciation, the allocations translated to approximately $13.7bn, representing $4.6bn decline in dollar value compared to the Buhari era.

Allocations to the 774 local government councils equally expanded sharply in naira terms but declined significantly in real value.

Local governments received N5.6tn during Buhari’s administration, equivalent to approximately $13.8bn.

Under Tinubu, allocations to local governments rose to N12.6tn, representing a 121.8 per cent increase in naira terms.

However, in dollar terms, the allocation amounted to approximately $10bn, reflecting a $3.8bn decline from the Buhari period.

The broader revenue profile of the federation account followed the same trajectory.

Further analysis showed that total FAAC revenue generated between May 2020 and April 2023 under Buhari stood at N30tn, equivalent to approximately $73.1bn using the average exchange rate during the period.

Under Tinubu, total FAAC revenue generated between May 2023 and March 2026 rose significantly to N86.1tn, representing an increase of about 187 per cent in nominal naira terms.

However, when converted using the prevailing exchange rate during the Tinubu administration, the revenue translated to approximately $67bn — about 8.34 per cent lower than the Buhari-era value.

THE WHISTLER findings suggest that while the Tinubu administration succeeded in expanding nominal government revenues through fiscal reforms, the accompanying collapse of the naira substantially weakened the purchasing power and real economic value of those revenues.

The trend has intensified concerns among economists and policy analysts over the sustainability of Nigeria’s public finance structure amid persistent inflation and exchange-rate instability.

The inflationary consequences of the reforms have been particularly severe for subnational governments whose infrastructure programmes rely heavily on imported inputs such as machinery, steel, petroleum products and construction materials.

With the naira losing more than two-thirds of its value against the dollar since the reforms began, the cost of executing public projects has risen sharply across the federation.

Several state governments have consequently reviewed contract values upward, delayed infrastructure projects or sought alternative financing arrangements to cope with escalating costs.

At the same time, governments have faced mounting pressure to increase workers’ wages and social spending as inflation eroded household incomes.

Despite these pressures, supporters of the reforms argue that the policy changes corrected longstanding structural distortions within the economy and placed government finances on a more sustainable path.

But speaking with THE WHISTLER, the Chief Executive Officer of the Centre for the Promotion of Private Enterprise (CPPE), Muda Yusuf, said the sharp increase in FAAC allocations reflected the combined effects of fuel subsidy removal and foreign exchange liberalisation.

According to Yusuf, exchange-rate depreciation contributed directly to the increase in distributable revenues because a large portion of Nigeria’s foreign exchange earnings is converted into naira before being shared among the three tiers of government.

He said, “Well, the impact is of course positive and negative. It’s positive in the sense that the exchange-rate reform, which also came with the depreciation, was part of the factors that led to the increase in the nominal amount of allocation that the states are getting. So, the exchange-rate depreciation has also boosted the FAAC allocation.”

He explained that subsidy removal and FX reforms jointly expanded revenues available for distribution.

“Two factors are responsible for the sharp increase in FAAC allocation. The first was the fuel subsidy removal. The second was the exchange-rate reform, which is also like removing the exchange-rate subsidy as well,” he said.

Yusuf, however, acknowledged that the same reforms also raised the cost structure of the economy significantly, especially for governments executing capital-intensive projects.

“The negative side is that it has increased the cost of projects, especially projects that have imported content,” he said.

“Many of the capital projects have import content. If, for instance, you are embarking on a project that should normally cost the government maybe $10,000, the naira value of that project would rise significantly after depreciation.

“So, in terms of the cost of projects, costs have increased significantly. To that extent, it’s also negative.”

He nevertheless argued that subnational governments were still financially stronger than they were before the reforms despite the inflationary pressures.

“But on the whole, even if we discount the depreciation and discount for inflation, the states are still much better off in terms of revenue than they used to have before the reforms of this administration,” Yusuf said.

According to him, the broader objective of the reforms extended beyond revenue generation to correcting structural distortions that had weakened investment and economic productivity for years.

“The way reforms are analysed goes beyond monetary value. It’s about correcting distortions in the economy. That is a major objective,” he said.

“It’s not so much about revenue because the exchange-rate structure or the foreign exchange policy before now had a lot of distortions, which were not only affecting government revenue, but the totality of the economy.”

Yusuf described the pre-reform foreign exchange regime as one that encouraged arbitrage and rewarded rent-seeking activities rather than productive investment.

“It was affecting investment because it created what you call a rent economy that enabled people to reap where they did not sow, suddenly become billionaires,” he said.

He also argued that fuel subsidy removal had improved fuel availability and reduced the chronic shortages that previously disrupted economic activity.

“Investors now have much better access to funds, and citizens also have much better access to petroleum products,” he said.

“Although the products have become expensive, the distortions and corruption they created have reduced. Citizens no longer have to experience anxiety about getting fuel or waiting in queues at fuel stations.

“Yes, the price of fuel has gone up, but you can plan your cash flow.”

Yusuf, however, cautioned against relying solely on dollar conversion to evaluate the real value of government revenues, arguing that such an approach may oversimplify the actual structure of costs within the Nigerian economy.

“Inflationary effect depends on the kind of project. Total dependence on dollar conversion may distort the picture,” he said.

“In this naira depreciation, not all costs went up in the same proportion. Some capital expenditure did not rise in the same proportion.”

He explained that projects with strong local content were less exposed to exchange-rate volatility compared to projects heavily dependent on imported materials.

“There are some costs that didn’t rise as much, especially costs related to local content in projects. Those costs did not rise as much as costs tied to foreign content,” he said.

“If you have road construction now, for instance, and you are using concrete roads, you are not importing too much bitumen, and most of your labour is local.”

Still, Yusuf acknowledged that inflation and exchange-rate depreciation had significantly reduced the real value of the higher FAAC allocations.

“That is why when people say governments are getting more revenue, we need to discount those revenues to accommodate inflation and the loss of value we are referencing, to arrive at the real increase,” he said.

“If you only look at nominal figures, it can give you a distorted picture of the increase in the real value of those allocations.”

Despite the economic pressures, Yusuf maintained that the reforms had produced a net positive fiscal outcome for state governments.

“The reforms that generated that additional income have also impacted costs. In nominal terms, the money has gone up, but costs have also gone up. However, the nominal value is still far ahead of the growth in costs. So, the net impact is still very positive,” he said.

Also speaking, a developmental economist, Afeez Balogun pointed to increased infrastructure spending and improved salary payments across many states as evidence that governments were financially stronger than before the reforms.

Afeez said, “That is why you will notice that many states are doing more projects than they used to do. If the net effect was not positive, they would not be embarking on so many projects.

“Many are not owing salaries, and they are not borrowing as heavily as the federal government. So definitely, the reforms have had a very positive impact on them.”

ENDS